Second Rate Cut & Stock Values

The Federal Reserve is set to meet next week and is widely expected to cut short-term interest rates. While opinions vary on how much they will cut, most analysts expect .25%, with the outliers being as high as .50% or as low as 0%. These meetings will likely affect markets for the foreseeable future.

The drumbeat warning of a potential recession has also grown louder following the yield curve inversion several weeks ago. It is difficult to ignore recession predictions considering that every recession since 1950 has been preceded by a yield curve inversion (however, not every inversion has been followed by a recession). While the evidence of a yield curve inversion preceding an economic recession and a related bear market is strong, like most things in the investing world, the timing of these recessions is unpredictable and can take years to play out. Because of the unpredictable timing, HCM has not yet taken its equity exposure below neutral levels; however, we have reduced our volatility through a recent equity reallocation. Offsetting economic risks is strong historical evidence that following a second rate cut (which is likely next week) on average, stocks enjoy significant gains over the following months.

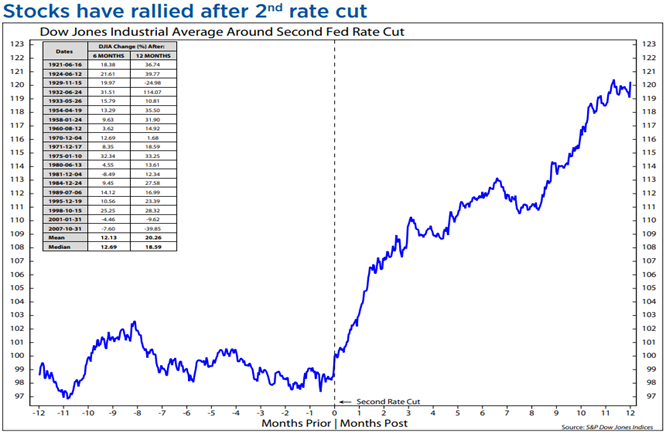

The chart above shows the average return for the Dow Jones Industrial Average 12 months prior to and 12 months after a second rate cut. After a second rate cut, the Dow has averaged a return of 20.3% one year later, according to a study by Ned Davis Research.

Why Do We Care?

While the data above is certainly encouraging for equity investors, the devil remains in the details. Even though most of the numbers for the time periods listed in the chart are positive, there are negative periods. These negative periods coincide with recessions and show an important distinction for those who want to sound the “all-clear” just because the Fed continues to cut rates. Recessions are the black hole from which nothing escapes, especially negative equity returns.

Just how big is the performance gap between recessionary and non-recessionary periods following a second rate cut? Further data from Ned Davis Research shows the average gain for the 12 months after the cut is 18.2% if the economy avoids a recession but drops to -10.8% if a recession hits.

With such a wide dispersion of possible outcomes, we can clearly see that historically the Fed has only so much ammunition to fight off recessions. We work through our portfolio designs based on the assumption that an economic recession would be the worst case scenario for HCM Clients. Fortunately, we don’t currently see hard data in the numbers that would indicate a recession is at our doorstep. One of the more reliable recession indicators, the Chicago Fed National Activity Index or CFNAI, remains above its recession reading despite indicating growth has slowed over the past several months. The CFNAI is a weighted average of 85 indicators of growth in national activity and has a successful track record identifying recessionary periods.

Despite not seeing hard evidence, we still need to be aware that risks remain in the market. The ongoing tariff issues between the US and China, collapsing interest rates around the globe and slowing growth projections all present headwinds to the market moving higher. Without these issues being resolved, HCM remains at neutral stock/bond weightings, with a slight bias towards high-quality, US assets. If we see a surprise from the Fed next week or a sudden spike in growth or inflation, the markets would likely see a resurgence in sectors such as value, small cap and emerging markets. We would also see a reversal in bond prices if growth were to surprise to the upside, as inflation would once again become a topic of discussion. Bonds have performed extremely well this year as inflation has been a no-show.

As we consider the possible outcomes from the upcoming Fed meeting, it gives us guarded optimism that a second rate cut will be a catalyst for higher equity prices. However, as past performance doesn’t guarantee future results, we will continue to plan for all possible outcomes so that HCM Clients will continue to enjoy secure retirements.

Weekly Focus – Think About It

“I don’t want to get to the end of my life and find that I have lived just the length of it. I want to live the width of it as well.”

-Diane Ackerman

Market Activity

Performance last week for the four major asset classes were:

- U.S. Stocks – Russell 3000 (IWV) – Gain of 1.74%

- Developed Foreign Markets (EFA) – Gain of 2.09%

- Emerging Markets (EEM) – Gain of 2.64%

- Fixed Income (AGG) – Loss of -.17%

(Note: performance is based on the change in price plus dividends)

Last Week’s Headlines

-Geopolitical risks continued to drive global markets. Asians stock rallied after Hong Kong’s leader promised to withdraw the extradition bill that had triggered anti-government protests.

-August ISM Manufacturing in the US dropped to 49.1, its first sub-50 level since August 2016, while August jobs growth came in below expectations. The ISM non-manufacturing survey came in above expectations at 56.4.

Eye on the Week Ahead

-The Federal Reserve will meet on Sept 17-18 and is expected to cut interest rates by .25%. Investors will pay close attention to the message delivered by Chair Powell around the possibility of further easing in the future.

If you have questions about the recent market conditions, please contact a member of HCM’s Wealth Advisory Team:

Disclaimer

Any tax or other advice contained in this document, including any attachments, is not intended and cannot be used for the purpose of avoiding penalties under Internal Revenue Code. No action should be taken on any information contained in this message without first consulting with your tax/legal advisors regarding the tax/legal consequences for your particular circumstances.

Additional Notes:

- The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

- Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

- Past performance does not guarantee future results.

- You cannot invest directly in an index.

- Consult your financial professional before making any investment decisions.

• • •